Fractional Reserve Banking Is Dead - And Banks Are Set To Cash In

Fractional Reserve Banking Is Dead - And Banks Are Set To Cash In

"The truth isn’t an easy pill to swallow, the truth that the fed rate is nothing more than interest the FED pays banks on your money so they won’t loan it out."

Fractional reserve banking has been practically dead for a while now, but officially deceased march 15th 2020. When the Fed announced that reserve requirements for all member banks would be set to zero. This isn’t a sellilique on the necessities of reserve requirements, but on something much more real, and pressing in the months to come.

That would be the “federal funds rate” which was once an integral part of that fractional reserve system, it has since been perverted into another giveaway for the rich.

Today, the ‘fed rate’ is no more or less than the interest paid to banks on balances held at the federal reserve. Threw what is called, unshockingly: Interest on reserve balances or (I.O.R.B). The ‘fed rate’ is money paid to banks in exchange for not loaning out your money.

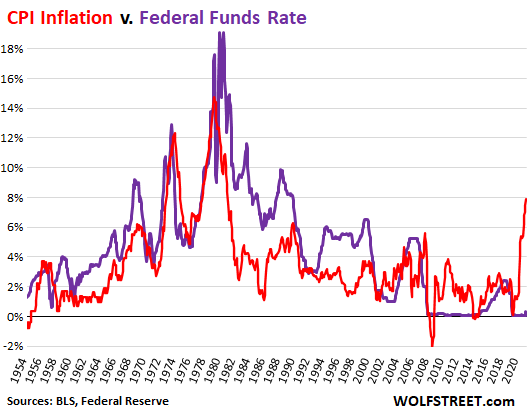

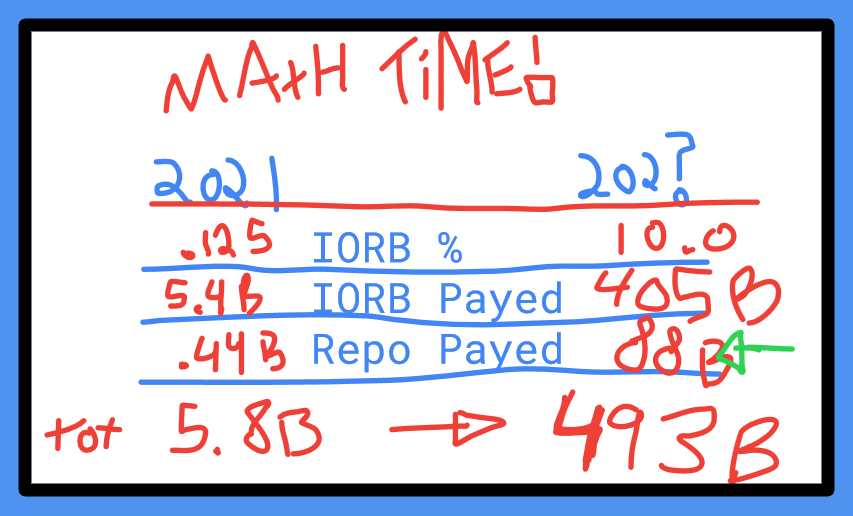

Looking at what the fed rate needed to be the last time we experienced inflation at this level. If the Fed actually chooses to move against inflation in a meaningful way, it will likely be paying the banks trillions of dollars to do it. But hey, don’t call it a subsidy.

And by the way, a monetary device that traditionally was used to restrict the creation of money, now actually creates money… Should work out fine.

HOW WE GOT HERE.

As I hinted at earlier, abolishing reserve requirements pre-dates the march 2020 announcement. Through accounts known as swaps, for decades, larger banks had been using a loophole to get around being constrained by reserves.

This is how the idea of paying IORB first came about - don’t fix the loophole, just use it as an excuse to make changes to the system. Because why force banks to not lend out money, when you can pay them to do it instead. The change in march of 2020 really only mattered to smaller banks - if it mattered at all.

IORB was already being planned before the 2008 financial crisis, but it wasn’t until the crash, and quantitative easing began, that it was implemented.

In a 2016 article, attempting to defend the policy, Ben Bernenke writes.

“without the ability to pay interest to banks the Fed would likely have to implement any tightening of monetary policy by rapidly selling assets it holds. This would have difficult-to-predict effects and would likely prove highly disruptive to financial markets, to say the least. ”

Article written by Ben Bernanke in 2016, attempting to defend the policy change.

The problem is bernanke is a true believer so he doesn't realize when he's saying the quiet part out loud. Protecting financial markets is priority one

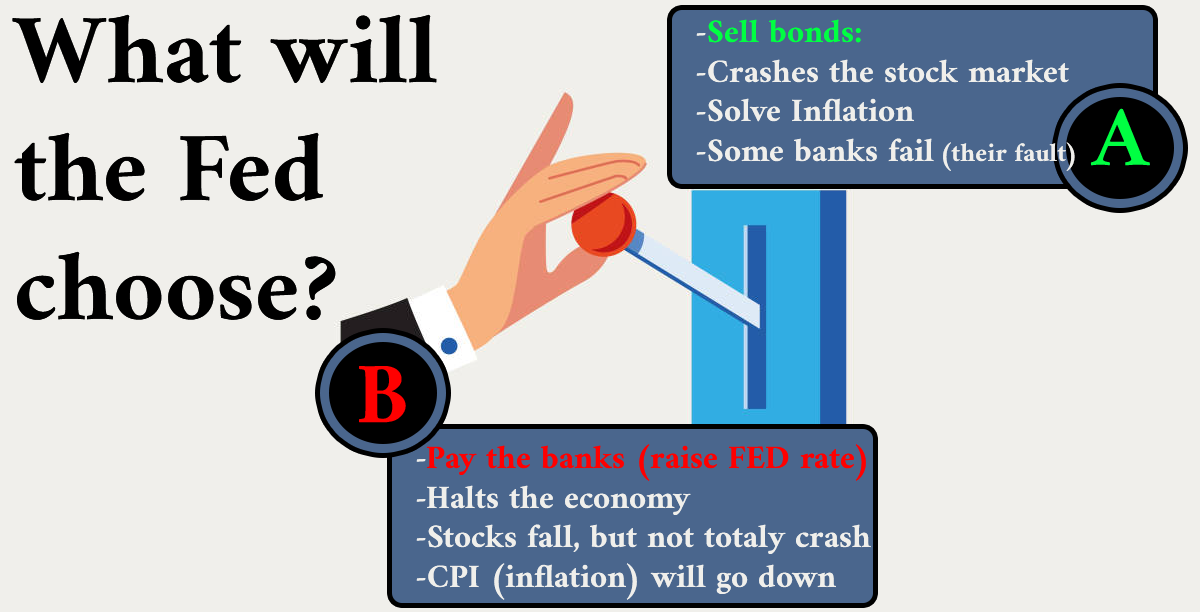

Fixing swaps and restoring reserve requirements, would mean that raising the fed rate, once again would involve the Fed selling bonds, in order to reduce excess reserves. Which once QE started, that would mean releasing the pressure it's kept on the treasury market. Which to bernanke, was totally unacceptable.

After-all, You can’t very well be selling bonds while you're buying bonds..

This is a good place to mention the reverse-repo market. I’m trying to paint broad strokes here, so the only thing I will say about it, is that the Fed has extended the IORB rate, actually just a few points lower than it, to any financial institution who can muster the minimum 1 million dollar bid for what are called repurchase agreements. So the windfall to come, won’t be restricted just to member banks but other financial institutions as well.

Traditional (old) definition for the Fed rate

Banks each have a minimum reserve, proportional to the deposits at their bank. This reserve requirement is held at a Federal Reserve. When a bank has excess reserves, it may lend them to banks that have a reserve deficit.

The fed rate is the rate at which banks lend their excess reserves to each other

The Federal reserve would change the fed rate by varying the amount of reserves each bank had (by replacing them with bonds).

Working As Intended.

So the Fed needed a way to slow down the economy in case it overheated, without directly affecting the amount of money in “financial markets”. And if some banks get paid a bit of money in the process, hey good times.

By separating the fed rate from bond transactions, they ironically created a method for reducing the money supply with mitigated effects on the actual economy. Though the whole point of separating them was to never have to do that, to never have to actually sell bonds.

In Bernenke’s article he worries that the Fed writing checks to banks might create a perception problem. Though it appears he worried for not - as barely anyone took notice. Though partially by design, I mean, the investopedia page for the fed funds rate, does not at all even mention IORB despite being updated 15 days before the recording of this video, 13 years after IORB was instituted. It does mention reserve requirements a few times, that's how you know you're looking in the wrong place. Don't trust that site btw.

Rather than varying the supply of reserves, the Fed now manages the federal funds rate by changing the rate of interest it pays on reserves -Bernenke

Inflation was solved in the early 80s with double digit fed rates. It was solved by limiting banks ability to create money, it also slowed the economy down in the process, but when dealing with stagflation, lowering the money supply is the much more important part of raising the fed rate - because the economy was never overheated in the first place, such is the nature of stagflation.

And therein lies the problem, the monetary device meant to restrict the creation of money, has been perverted into just another method to create it.

YouTube video of this story is here.

-Casey Lee.